Micro suites are becoming the latest rage in urban development. Even in our small city of 200,000 people, micro suite living is becoming a reality and a choice for those looking for hamster-sized accommodations. There’s a number of micro suites projects completed with more to come:

No, it’s not the fact that less than a month away people down south will have to choose between Hilary Clinton and Donald Trump. I actually don’t care much for politicians except for times when they’re handing out free sandwiches in my general vicinity. Rest of the time they’re fairly useless in improving lives of general population, so why bother pay attention to them.

No, what’s really sad and depressing is rising real estate prices in Canada.

Even though prices seem to be stabilizing and in some places going down, real estate prices in Canada are still outrageously high. Average price of a detached house in Vancouver after a major sell-off is sitting at cool $1.5M. Oh my, what a bargain! Not really.

Doesn’t get much cheaper if you pick Toronto - average detached house will set you back roughly $1.3M. Calgary? Around one million. Kelowna, BC where we call home - about $700,000. Yes, much cheaper than Vancouver where we lived for a bit, but keep in mind that incomes around here are much lower as well.

At first glance, mortgage life insurance obtained from your bank sounds like an excellent idea. You’re buying a home for your family and sign up for a loan that will take decades to repay. While you’re signing documents for your mortgage, your bank rep mentions the benefits of getting mortgage life insurance - peace of mind, complete repayment of your mortgage in case you or your spouse pass away, and relative low cost (when compared to your mortgage amount that is). Sounds like a responsible thing to do to protect your family, right?

Mortgage Life Insurance

When we bought our home few years ago, we had this exact conversation with our mortgage specialist. Fortunately, I had enough brain cells to say that I needed more time to research it, and I started digging around. After looking into details of the mortgage life insurance offered by the bank, I found several reasons why it’s an awful product, and should be avoided at all costs - unless your hobbies include wasting money.

Mortgage life insurance is too expensive

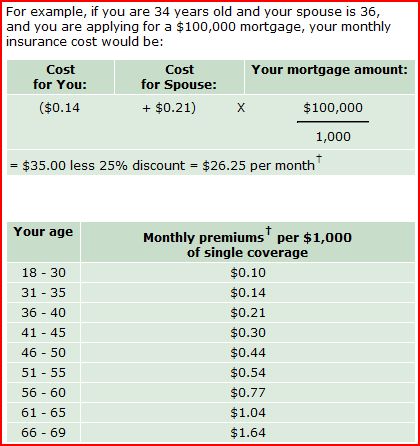

Just out of curiosity, I’ve looked up the cost for mortgage life insurance on TD Canada Trust website. For example, you’re buying a small house and taking out a mortgage of $400,000. To obtain life insurance for a mortgage of this amount, you and your spouse (in my example you’re in your 30s) will have to pay $105.00/month (after generous 25% discount). If your mortgage amount is higher or if you and your spouse are older, the monthly expense will be higher.

Mortgage Life Insurance

This is extremely expensive when compared to simple term life insurance that can be obtained through independent brokers. Similar coverage of term life insurance would cost you less than $40/month and offer more to you - as I discuss it late. Even our life insurance policy offers superior coverage and flexibility.

While $105.00/month might not seem like a big deal when compared to your mortgage payment, the value just isn’t there. Also, keep in mind that your coverage will be going down as your mortgage is being paid down - while your premiums will stay the same.

No guarantee of paying out

Typical life insurance policy obtained through insurance broker is actually underwritten when you sign the contract and the risk is assessed prior to this. Once you enter the contract, the payout is guaranteed in case you or your spouse die. Insurance agencies take this step very seriously, and take every step possible to assess your health before the policy is signed. In our case, we had to go through a medical examination performed by a registered nurse to make sure our level of health is reasonable and we are insurable.

Mortgage life insurance is a bit different in a sense that it’s underwritten at the time of the claim. Bank won’t access your health prior to signing the documents; you simply fill out a short questionnaire about your health. If the unthinkable happens, the bank can actually deny the coverage simply because you weren’t insurable. The fact that you didn’t know about your heart condition won’t make any difference.

Check out this episode of CBC Marketplace on mortgage life insurance:

Mortgage life insurance is controlled by the bank

If I had mortgage life insurance for our home, and got hit by a bus, the payout would go straight to the bank holding my mortgage because the bank is the beneficiary for the insurance policy. My wife wouldn’t be able to make a choice on what to do with insurance money - it would simply pay off our mortgage. In case of private insurance, the proceeds would be given to my wife tax free with her choice of actions - pay off the mortgage, invest the money, or build a giant Rocky-styled statue of me.

Another thing to keep in mind is that your mortgage life insurance policy is attached to your mortgage. If you sell the house - the policy gets canceled. If you renew the mortgage - the police needs to be renewed. If you miss a payment - your policy gets compromised. In other words, you have no control over it whatsoever.

Why do banks offer mortgage life insurance?

Mortgage life insurance is an easy sell for bank employees to push to their clients as an added bonus. Any responsible adult would think about protecting their family from unexpected death. But mortgage life insurance offered by most banks is not the right way to do so. In reality, it protects the banks more than it protects you. It is also a great money maker for them given extremely high price and poor value of it to the consumer. No wonder bank employees are told to push this awful product!

What is the right way to go?

Don’t get me wrong, protecting yourself and your family is important and insurance can be a beautiful thing. It is your responsibility to make sure your family won’t suffer financially if you or your spouse suddenly passes away.

But mortgage life insurance offered by the banks is an awful product that offers very little value. If I were you, I’d consider obtaining term life insurance from an independent insurance company. You will be able to control the coverage amount and what happens if the policy pays out. Your premiums will also be much lower than what the bank will offer you - and who can’t use some extra money these days?

My name is Financial Underdog, and I’m not impressed with mortgage life insurance!

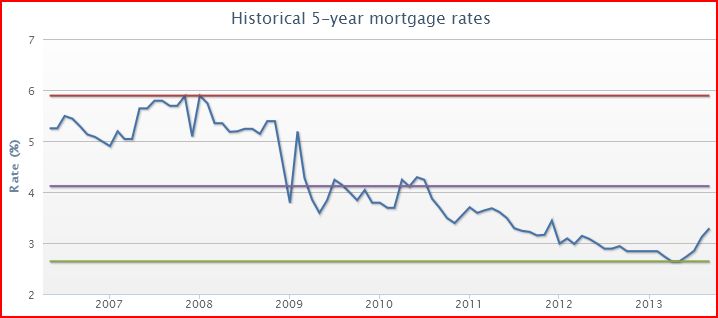

Rising mortgage rates in have been discussed for quite some time. As you may or may not know, mortgage rates in Canada are tied to Bank of Canada lending rate - banks borrow their money from Bank of Canada, and then turn around and lend money to you and me. Of course, they charge a bit extra - after all, they’re in business of making money, not simply passing it around. Once you understand this, it’s easy to understand that Bank of Canada lending rate is tied to mortgage rates in general. If Bank of Canada brings their rate up, almost all banks follow the trend and raise their rates - because they don’t want to lose money. Three days ago, Bank of Canada made an announcement that interest rates will be staying where they’re now for now.

Rising Mortgage Rates in Canada

But it’s important to understand that currently mortgage rates (and other lending rates) are at historical lows. If you ever talk to old-timers, they’ll remember the rates being in double digits - 15-20%. Rates have been falling over the years - and with last recession Bank of Canada cut them to never-seen-before levels. Where will they go from here? I think it’s safe to say that they have nowhere to go but up. The economy is coming around, and sooner or later our government will have to do something to prevent it from running away again - and interest rates is one of the ways control it.

What are you paying now in interest?

If you ask somebody about their mortgage rates, they’ll probably respond “Oh, I’m paying around 3% currently”. People who pay a bit more attention to their finances will say “My monthly mortgage payment is $1200”. Somebody who is borderline obsessed with personal finance (that would be me) will say “My by-weekly mortgage payment is $495.17, and I pay my bank 3.89%!”.

Your mortgage payment consists of two parts - principal repayment (amount that goes towards paying off the house) and interest payment (amount the bank gets for lending you money). Lumped together is the amount leaving your bank account every month (or by-weekly if you’re on by-weekly payments). If you ever want to get depressed quickly, ask your bank how much of that amount is interest and how much goes towards the principal. Just because I had nothing to do, I called my bank:

Good god, somebody give me some wine. My mortgage payment is mostly interest charges! No wonder banks have such nice buildings.

What happens if the mortgage rates double?

Currently we’re paying 3.89% on our mortgage - which was a good rate when we bought our little home, not so good right now. Historical average for mortgage rates over the last 30-40 years is actually closer to 8 percent, or roughly double what it is right now for us personally. In two years, we’ll have to refinance our mortgage since our 5-year term will be up - but what kind of rate will we get? And with all the talk about rising mortgage rates in Canada - I got curious and decided to do some math.

Quick and dirty math on our mortgage payment if our rates double. The real number would be slightly off - because by that time our mortgage amount would be lower but that’s why I call it quick and dirty:

Good god, I need more wine. If the interest rates indeed double in two years, our mortgage payment will be over $800 (by-weekly) - which means we’ll be paying over $1600/month.

Can we afford it? Well, it will certainly put a break on our saving rates - currently we’re saving quite a bit for the future as many financial advisors recommend. If the mortgage rates double (and I doubt our income will do the same thing unless I start removing my clothes for money), most of the increase will have to come from the money we’re currently saving. The result? Less money being saved for the future, less money for consumption, and a whole lot of wine being bought.

How will rising mortgage rates affect you personally?

Ask yourself few questions - what is your current mortgage rate? How much are you paying in interest and principal payments? What happens if mortgage rates return to their historical average, will you be able to afford your house? Will you have to adjust your life?

While many people might be scared of rising mortgage rates in Canada, one thing you can do to punch fear in the face is to educate yourself. At least once you know your situation and facts, you can make an educated decision to worry about them - or not.

Once you educate yourself, you can look at some options - refinancing your mortgage to lock into current rates or even extending your mortgage term to 10 years. You can also increase your current principal payment and accelerate your mortgage repayment - this way your principal amount is lower when you’re refinancing.